BAM Fund-raising: Strong Words, Weak Results

Fund-raising in its core investment silos has declined materially since 2022. Infrastructure realizations on a y/y basis are troublingly low.

Brookfield Asset Management’s (BAM) 4Q24 conference call boasted of earnings and AUM growth, and accelerating asset dispositions. Management’s emphasis on fund-raising and monetization dovetailed well with our interests. In a recent note, we questioned whether slow dispositions in private infrastructure funds are indicative of inflated returns, and may potentially impede capital raising.

Today, we look at longer-term fund-raising trends in BAM’s core private investment silos. We also take another look at infrastructure monetizations, comparing changes in realized returns from 4Q23 and 4Q24.

The numbers contrast sharply with the boastful confidence displayed on the call:

Fundraising in core silos (ex-Oaktree) was down -67% in 2024 vs 2022.

New analysis has confirmed our opinion that infrastructure realizations are sub-par. Analysis in a year-over-year framework shows that realizations in the segment were a paltry ~$3B, only 11.7% of the balance of the three oldest funds.

A recent article in the Wall Street Journal, discussed issues facing private equity firms, which includes both fund-raising and asset dispositions. The article classifies Brookfield as a “have” in an industry of have and have nots, but analysis shows a different reality. Excluding the Oaktree contributions, Brookfield appears to be a microcosm of everything plaguing the industry.

Rhetoric and numbers

Not one to mince words, this is how Bruce Flatt kicked-off the conference call:

Never Been Better?

Source: 4Q24 conference call transcript.

BAM includes Oaktree capital raising in its results, though it does not own 100% of the company. We wanted to see how BAM’s capital raising is doing in its original business. To do so, we extracted the net change in fee-bearing capital for BAM’s core silos from the quarterly supplemental.

The results do not corroborate Mr. Flatt’s statements, as shown in the table below.

BAM’s capital raising prowess in core PE markets appears to be on the wane, declining -66.8% overall from $43.5B in 2022 to $14.4B in 2024. While there may be some variation driven by the type of funds raised, BAM has been in constant capital raising mode over the entire period, suggesting the impact of fund-type may be limited.

BAM had two vintage funds in each year from 2021 to 2024. Infrastructure and private equity have raised one fund each, renewable and real estate three each.

Capital raising in infrastructure has collapsed, despite having raised a flagship fund in 2022, of which approximately ~40% of the $27.5B has been drawn down. Renewable has raised three “transition” funds. The absolute dollar amounts are low by BAM standards. Given the modest success of the funds, one has to wonder how fund-raising will be going forward for “transition” given the dramatic change in the political environment?

Fund-raising in core silos was terrible in 2024 excluding Oaktree, in our view. Oaktree’s credit business may have saved the day, but BAM’s private market products are extremely weak. Of particular note is how far the once mighty real estate and infrastructure segments have fallen.

The WSJ article notes that Blackstone expects its next large PE fund to be smaller than the last. Given what we view as persistent realization issues in infrastructure and obvious troubles in real estate following the failure of BPY, we would be surprised if BAM funds do not shrink as well.

Infrastructure realizations – still sub-par

Mr. Flatt’s second point was that firm-wide monetizations in the year were very strong. Our earlier report noted the low level of realizations compared to competitive funds in the infrastructure silo. In the table below, we show changes in realizations for BAM’s infrastructure funds over 2024. We don’t see any evidence that the infrastructure silo participated in the “strongest year across the board” with respect to investment realizations.

BIF I’s realized returns actually declined. This reflected what we estimate to be strong (~18%) booked returns in the fund. So, while realizations were positive in the year, there was a net increase in total value, lowering the realized gain percentage.

Realizations of the 2013 and 2016 vintage funds changed only modestly, which is particularly concerning for BIF II, which is 11-years old and should be in full liquidation mode. BIF II increased to only 53% from 47% at the end of 2023.

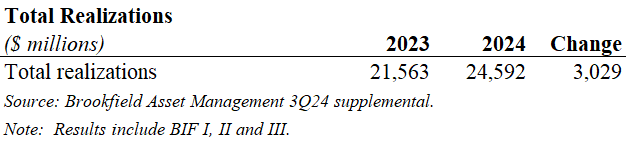

The figures indicate slow realizations. The absolute dollar amounts, below, show just how sluggish they are.

Total realizations for the three funds listed above were just over $3B for the year, only 11.7% of the beginning unrealized balance for BIF’s I to III.

The number is more troubling if one considers only BIF I and II. The funds are 15 and 11-years old, respectively. At the end of 2023, the funds had combined unrealized gains of $8.756B and realized only $1.475B or 16.8% of the remaining portfolio.

In BAM’s 2023 annual report, the firm notes that private funds are typically committed for 10-years with two 1-year extension options. BIF I is far beyond those parameters and BIF II is close to the outer limits. Current trends in realizations suggest that it may take 15-20 years to fully liquidate what should be 10-year funds. We would be surprised if allocators didn’t come to the same conclusion.

Sunset on Private Equity?

In our experience, it can be difficult to get a full picture of business performance at Brookfield companies from management commentary on conference calls. The company line is one thing, but data is another. Details matter and, as shown here, analysis can provide a strong counter-point to management’s presentation.

In this case, BAM’s long-term fund-raising data in core private markets and issues realizing gains in infrastructure funds are less supportive of the ‘strongest year across the board’ claims, and more supportive of the WSJ article’s implications that the golden years of PE may be coming to a close.Total realizations for the three funds listed above were just over $3B for the year, only 11.7% of the beginning unrealized balance for BIF’s I to III.

The number is more troubling if one considers only BIF I and II. The funds are 15 and 11-years old, respectively. At the end of 2023, the funds had combined unrealized gains of $8.756B and realized only $1.475B or 16.8% of the remaining portfolio.

In BAM’s 2023 annual report, the firm notes that private funds are typically committed for 10-years with two 1-year extension options. BIF I is far beyond those parameters and BIF II is close to the outer limits. Current trends in realizations suggest that it may take 15-20 years to fully liquidate what should be 10-year funds. We would be surprised if allocators didn’t come to the same conclusion.

Sunset on Private Equity?

In our experience, it can be difficult to get a full picture of business performance at Brookfield companies from management commentary on conference calls. The company line is one thing, but data is another. Details matter and, as shown here, analysis can provide a strong counter-point to management’s presentation.

In this case, BAM’s long-term fund-raising data in core private markets and issues realizing gains in infrastructure funds are less supportive of the ‘strongest year across the board’ claims, and more supportive of the WSJ article’s implications that the golden years of PE may be coming to a close.

APPENDIX