Brookfield's Real Estate Silo is Broken

In this far from comprehensive review of Brookfield Property Partner’s 2023 20-F, disastrous financial performance and copious related-party transactions with cryptic counterparties are key themes.

Brookfield Property Partners (BPY), the now wholly-owned subsidiary of Brookfield Corp (BN) had a difficult year. It would have been a catastrophic year for an independent entity, but Brookfield is a group and one hand washes another. Related-party dealings are now a defining feature of the entity.

The “meta” implications of the poor financial performance are important, in my view. BPY consolidates the old Brookfield Office Properties’ core portfolio along with many BAM-managed funds, which own assets including the mall portfolios of both Rousse Properties and GGP. It’s amalgamated financial performance should be a reasonable representation of Brookfield’s real estate silo as a whole. The IFRS statements show an unmitigated disaster, where NOI no longer covers interest expense. Leverage is a problem.

I am well-aware of the fact that Brookfield is attempting to raise a new $15B fund, and it has already raised around half at $7B (including Brookfield commitments). I find it difficult to reconcile institutional willingness to invest in Brookfield funds with what I see filed with the SEC. Either institutions have a different perspective on the numbers or there are other factors at play.

I. Dead Funds Limping

We have all heard Brookfield management talk about how the real estate market has bifurcated and top quality assets are performing and the other is not; and how Brookfield’s assets have been outperforming despite headwinds. This is what outperformance looks like from an audited IFRS financial point of view.

For our purposes here, I eliminated revenues and expenses not directly related to real estate.

Total revenue increased almost 40% over the period; adjusted NOI lagged at 27% growth. A 470 basis point decline in NOI margin from 52.7% to 48.1% was the culprit there.

The interest expense increased 86% over the period shown on an absolute basis. As a percentage of NOI, interest expense increased from 81% to 118%. I estimate the average cost of debt to have risen from ~4.7% to 7.6%.

BPY would clearly not be viable as an independent entity. BPY is broke, with negative cash flows before general and administrative expenses. Adding $1.4B in G&A to the ($726M) of after interest NOI brings the basic losses to ($2.1B) for the year.

BPY always suffered from excess leverage, but the rapid raise in rates lit the fuse of the debt bomb. Amplifying the immediate problem of the interest expense, which increased from $2.6B to $4.8B since 2020 is the $28.7B, or 42% of total consolidated debt, due in 2024. The 20-F says that Brookfield expects to be able to “refinance or exercise options to extend” near-term maturities. Despite Brookfield being a large, well-respected investor, that strikes me as a tad optimistic.

Viewing performance on a segment level shows the proportional results and the growing pain over the last few years. The exhibit below for summarizes the results.

FFO declined in each segment for a total of $902M since 2021. Leverage is the problem, as exhibited by the bottom panel showing interest expense as a percentage of EBITDA. It started from a high 82% in 2021 and grew to 107% in 2023.

In my view, the evolution of finances makes two key points. BPY would be bankrupt as an independent entity. The real estate portfolio has been blown-up by extracting too much cash and layering on too much debt. It’s not too different from the blow-up in the early 1990s.

It also shows that the LP Investments is the most highly levered and worst performing segment. The segment represents the performance of the BAM-managed funds. The reported fund IRRs in supplementals looks ok, in contrast to what is visible here.

What I always disliked about analyzing BPY is the fact that the IFRS financial statements do not represent the interests of what were public limited partnership units. However, what I find very useful about the BPY filings is that it includes assets across Brookfield’s real estate empire.

The 2023 statements indicate that Brookfield’s real estate silo is an over-levered financial wreck.

Consolidated entities made a total of $4.7B in distributions in 2023, $3.4B of which went to non-controlling interests, which should be other Brookfield investors, such as private funds.

The 20-F says that the gap between distributions and cash flow from operations ($670M), which amounts to a cash deficit of ($5.3B) was funded with asset sales. However, the cash flow statement show acquisitions exceeding dispositions by ~$3B. The obvious question is: how were these transactions financed?

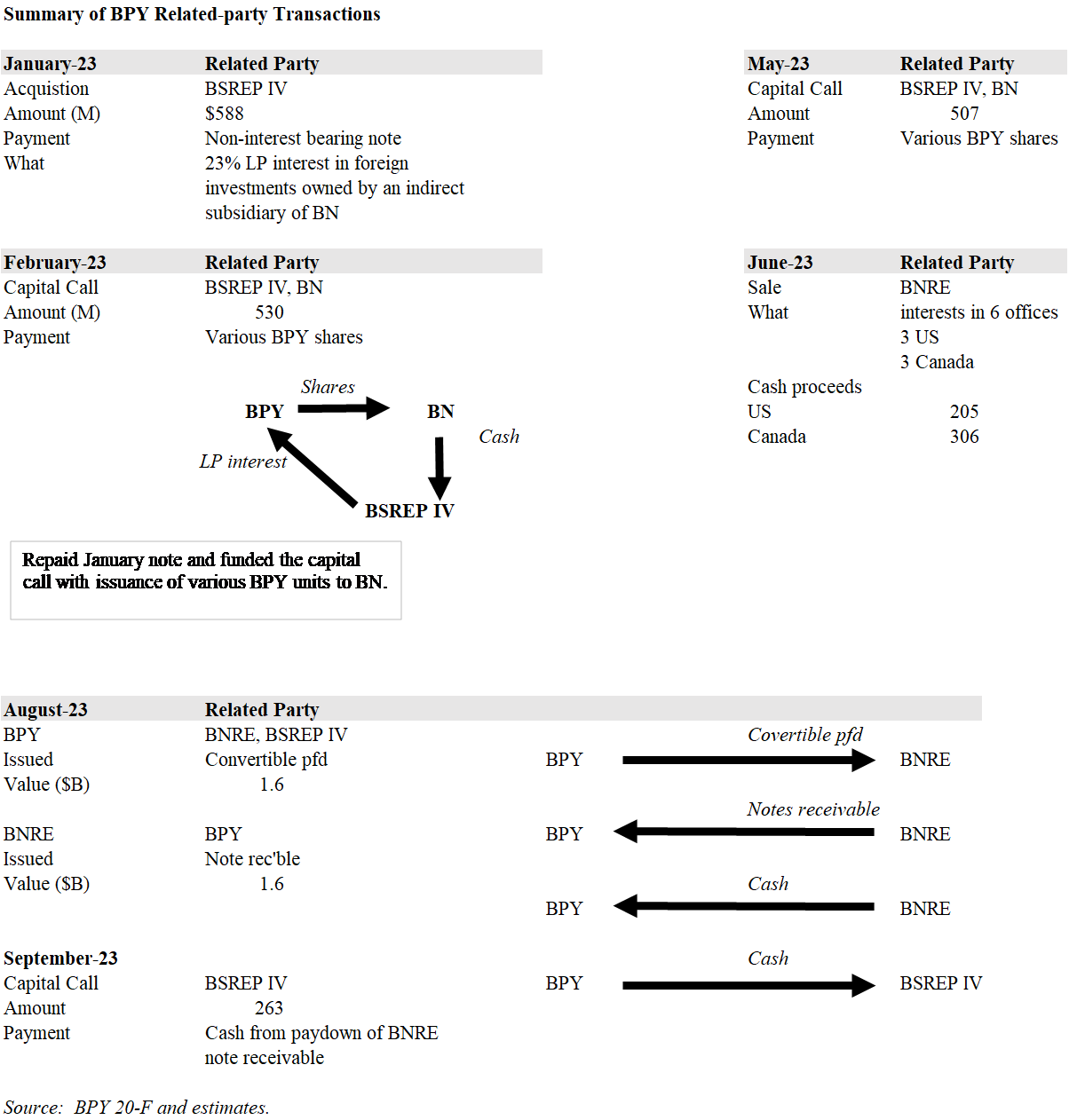

II. An Orgy of Related-Party Dealings

BPY’s financial statements are dominated by related-party transactions. Below we have provided a summary of transactions taken from the 20-F. BPY purchased assets, sold assets, issued and received various forms of script – all to and from related-parties.

To be frank, count me as impressed. The volume and complexity of these related-party transactions amount to an accounting tour de force. There is so much paper and cash criss-crossing this dense web of transactions, one must commend the spread-sheet jockeys for keeping it all straight. Further, the conflicts are so severe as to make it hard to believe it is legal in a regulated business – but there it is in “full-view”. I don’t doubt that they pass regulatory muster. Quotations are used because, as becomes clear below, the disclosure has some pretty severe limitations that should set investors’ spidey-sense tingling.

Here is my list of the transactions. I created diagrams for some in effort to figure out what was happening. Hopefully, they are accurate and help you, too.

One recurring theme in the transactions is the struggle for BPY to meet its commitments to participate in the BAM-managed funds. We see this in both capital calls and the August transaction with BNRE – Brookfield Reinsurance.

BNRE has emerged as a key new source of capital, providing liquidity to other Brookfield entities in a crippled CRE market that has exhibited collapsing pricing in some metro areas. I consider controlling both the buyers and sellers quite a competitive advantage.

Questions arising from the disclosures include: what were the BSREP IV “foreign investments” BPY bought, and from which indirect BN subsidiary? Why the cryptic reference to both assets and the counterparty? Language describing the seller is so vague as to be meaningless. Is the indirect subsidiary owned by BN or controlled? Did BPY bail out a fund or third-party investor out of, say, a position in the German Alstria Office REIT, which Brookfield acquired just prior to collapse?

When you get down to it, investors have no idea what happened. We don’t even know what foreign means. BPY presents itself in the 20-F thusly: “Our company’s head and registered office is 73 Front Street, 5th Floor, Hamilton HM 12, Bermuda, and our company’s telephone number is +441 294 3309”.

I believe that when a US-based or Canadian company cites “foreign” it means outside their home base. However, I think there is a 99.9% chance that “foreign” does not mean non-Bermuda. What does it mean and how would we know? Guess? My guess is that BPY acquired European assets, given that geographical zone has the largest year-over-year change in assets.

One related-party transaction that heavily influenced 2023 financial statements actually occurred in December 2022. It involved BPY’s purchase of “certain LP interests” from BN for a net consideration of $2.5B paid for with shares.

The “Manager Reorg” as it is called, is referred to throughout the 2023 20-F in connection with various significant financial changes. Despite the large price-tag and impact on the financial statements, investors are given no meaninglful information on the transaction. The 2022 20-F describes the deal in one paragraph totaling 75 words, which are repeated throughout the report.

When you really read and consider what Brookfield is saying in these disclosures, you begin to realize that they are empty. Brookfield has perfected the craft of information-free disclosure, in my view.

BPY provides a table that gives a nice summary of balances outstanding with related-parties. I think it is very instructive to look at the data over time, which I show below.

The clear overarching conclusion here is that BPY has become entirely reliant on related-party financing. Interestingly, it seems related-parties even provide entities consolidated by BPY with mortgages, which is highlighted in the table above. My interpretation is that maturing debt could neither be refinanced with third-parties nor repaid; related-parties stepped in preventing default.

In my view, a key question is who are the ultimate counterparties in these related-party transactions? For example, who is providing property specific debt to BPY and/or the funds consolidated? Is it a BAM-managed private fund, an Oaktree debt fund, BN itself? Does anyone outside the inner circle within Brookfield know? The property debt, corporate borrowings and loans and notes receivable could come from any number of Brookfield controlled entities, directly or using BN as an intermediary.

This is important for two reasons. I wonder if investors know how their capital is deployed? To illustrate with a hypothetical example – if an Oaktree fund provided the mortgages, did investors know or imagine their capital would be used to finance over-levered related-party properties?

These related-party transactions are evidence of something I have always found deeply troubling about Brookfield: from the outside it looks like capital is raised with debt and equity offerings from institutions and retail, across public and private vehicles, and it all goes into one giant pot. Capital in hand, management then seems to do whatever it wants with it.

In my imagination, I see Brookfield accountants breaking-out their spreadsheets, furiously drawing boxes and arrows, shuffling assets, cash, notes, loans, preferred shares, LP interests and seemingly every form of script known to man across the board until things balance and all parties show a profit – on paper.

After reading your post, I spent a fair amount of time trying to understand this myself. What a nightmare. It will be interesting to see Q1 when BPY posts Q1 and the numbers should be cleaner. Still going through the filings....

Great work!